")

Back to Journals » Advances in Medical Education and Practice » Volume 15

Integrating a Personal Finance Workshop to Enhance Financial Literacy Among Senior Medical Students: A Single Institution’s Experience

Authors Woolley PA, Kendall MC , Tacvorian S , Asher S

Received 25 June 2024

Accepted for publication 15 September 2024

Published 25 September 2024 Volume 2024:15 Pages 885—891

DOI https://doi.org/10.2147/AMEP.S474002

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Md Anwarul Azim Majumder

Parker A Woolley,1 Mark C Kendall,2 Simon Tacvorian,2 Shyamal Asher2

1Department of Anesthesiology, Critical Care and Pain Medicine, Beth Israel Deaconess Medical Center, Harvard Medical School, Boston, MA, USA; 2Department of Anesthesiology, The Warren Alpert Medical School of Brown University, Providence, RI, USA

Correspondence: Shyamal Asher, Email [email protected]

Purpose: Graduating medical students frequently start their training burdened with substantial financial debt and minimal savings, especially in comparison to their peers in other professional fields. A lack of financial literacy can result in increased debt, decreased job satisfaction and contribute to physician burnout. Enhancing financial education could improve both the financial stability and emotional well-being of future medical professionals. In this study, a basic personal finance workshop was conducted for 4th year medical students at a single institution. The aim of the study was to determine the impact of the personal finance workshop on improving financial literacy.

Methods: An introduction to basic personal finance workshop was open to enrollment for all 4th year medical students at The Alpert Medical School at Brown University. A 40-question survey to evaluate financial literacy was administered to all participants before and 6-months after the workshop. The topics covered included student loan management, basics of retirement accounts, investing, budgeting, saving and consensus surrounding financial topics. The results were analyzed using student paired t-test and Chi-square test of independence.

Results: Overall, an improvement in financial literacy was reported 6 months after the personal finance workshop (62% vs 54%, p = 0.004). Students subjectively reported an increase in confidence in their personal finance knowledge (16% vs 44%) and general knowledge regarding retirement savings (7% vs 55%). More than 92% of students agreed or strongly agreed that a basic personal finance education should be included as part of the medical school curriculum.

Conclusion: A personal finance workshop for medical students nearing graduation increases awareness and confidence in financial knowledge. The incorporation of basic financial education in the medical school curriculum may help young physicians establish better financial habits that will improve their financial wellbeing.

Keywords: financial literacy, finance, medical student, retirement

Introduction

Throughout the course of pursuing a career in medicine, medical students accumulate a substantial amount of educational debt and have little or no savings or assets at graduation. Following graduation from medical school, young physicians enter graduate medical education training programs that average three to seven years depending on the chosen specialty. During this time, debt payments are frequently deferred until after the completion of medical training. As a result, it is not unusual for the average medical school graduate to owe four times more than the average college graduate.1 Increased financial burden is associated with lower mental well-being and reduced academic and clinical performance, which could potentially jeopardize patient care.

United States medical schools have increasingly promoted medical student well-being by providing resources that often lack basic personal finance literacy.2,3 According to the 2023 AAMC Medical School Graduation Questionnaire the median medical student educational debt is $200,000 in the US.4 Poor financial literacy has been shown to lead to deleterious effects on psychosocial health and financial well-being.5,6 This combination of limited financial literacy and rising debt has been linked to increasing physician burnout and negative effects on clinical and academic performance.7,8 A large national survey in which more than 16,000 internal medicine residents reported that greater education debt was associated with at least one symptom of burnout and lower In-Training Exam scores.8 A more recent survey from physical medicine and rehabilitation residents revealed that more than 75% of the survey responders reported minimal financial education, leading to financial strain and negative effects on their mental health. Moreover, eighty five percent of responders wished they received more formal education in personal finance management. It is not surprising that most of all the responders (93%) believed they were poorly prepared to effectively manage their finances.6

Medical school at Brown University entails expenses comparable to those at other private US medical schools, with students experiencing substantial tuition and living costs that lead to similar financial challenges. Medical students at Brown University are offered multiple asynchronous and in-person workshops to earn credit to graduate and to prepare them for their internship. However, none of those workshops provide any formal personal finance education. To fill this void, the authors provided a commercial-bias-free workshop in basic personal finance topics to 4th year medical students as part of the Internship Preparation Course (IPC). The topics covered ranged from student loan management, basics of budgeting and saving, investment and asset protection concepts, subjective emotions surrounding finances, and retirement strategies. The purpose was to determine the impact of this personal finance workshop on improving financial literacy among fourth year medical students at the Warren Alpert Medical School of Brown University. In addition, we sought to know whether this cohort of students, as interns, initiated basic financial planning involving retirement accounts, emergency funds and insurance.

Methods

The Rhode Island Hospital Institutional Review Board determined that this study is exempt from Human Subjects Research under 45 Code of Federal Regulations 46.104(d) requirements and does not require consent documentation (IRB# 1842335). Participants received an introductory letter describing the nature of the study and their completion of the survey indicating their willingness to participate in the study.

Participants

The workshop, “Financial Management for Graduating Medical Students”, was open to enrollment for all fourth-year medical students at The Alpert Medical School at Brown University. Medical students who registered to participate for the personal finance workshop were invited to complete an anonymous web-based survey administered by SurveyMonkey.

Personal Finance Workshop

The medical students have a number of workshops to choose from, and self-select 5 out of 20 workshops to earn credit for IPC which is required for graduation. The personal finance workshop was held in the spring semester and consisted of 3 hours of in-person instruction given by the senior author (SA) who is experienced in personal finance. The workshop consisted of traditional lecture-based teaching, interactive in-class exercises, and Q&A discussions. The topics covered included student loan management including repayment strategies; public service loan forgiveness (PSLF); refinancing options; saving for retirement including retirement plan overview; basics principles of investing and choosing investments; budgeting and saving strategies; and basic behavioral economics as applied to personal finance.

Survey

The survey consisted of 40 questions and was categorized into 6 subsections of: Demographics (9), Financial Planning (3), Savings (2), Student Loans (1), Financial Literacy questions (18), and Consensus Surrounding Financial Topics (7) (Appendix A). The responses were in the form of multiple choice with the option of selecting “prefer not to say” or “unsure”. A 5-point Likert scale (agree/disagree) was used for answers pertaining to questions regarding financial topics. The questions for assessing financial literacy were adapted from the Financial Industry Regulatory Authority (FINRA), who granted permission for use in publication.9 These questions have been used in other medical student and resident financial literacy studies.10

Six-months after the workshop was completed, the participants, who were now PGY-1 residents in their respective residency programs, were contacted via Email to fill out a follow-up post-workshop survey. Participation was voluntary. We chose a six-month period for post-workshop evaluation to provide enough time for participants to interact with their financial resources at their respective institutions. To encourage participation, a $10 electronic gift card was offered to participants that completed the post-workshop survey. The post-workshop survey contained 8 additional questions on the implementation of basic financial strategies that were presented during the workshop (Appendix B). Three reminder emails were provided and the survey remained open for a total of 4 weeks. The survey took less than 10 minutes to complete. All analyses were performed using Stata/SE 17.0 (StataCorp LLC). The results were analyzed using student paired t-test and Chi-square test of independence. P values of <0.05 were considered statistically significant.

Results

Demographics

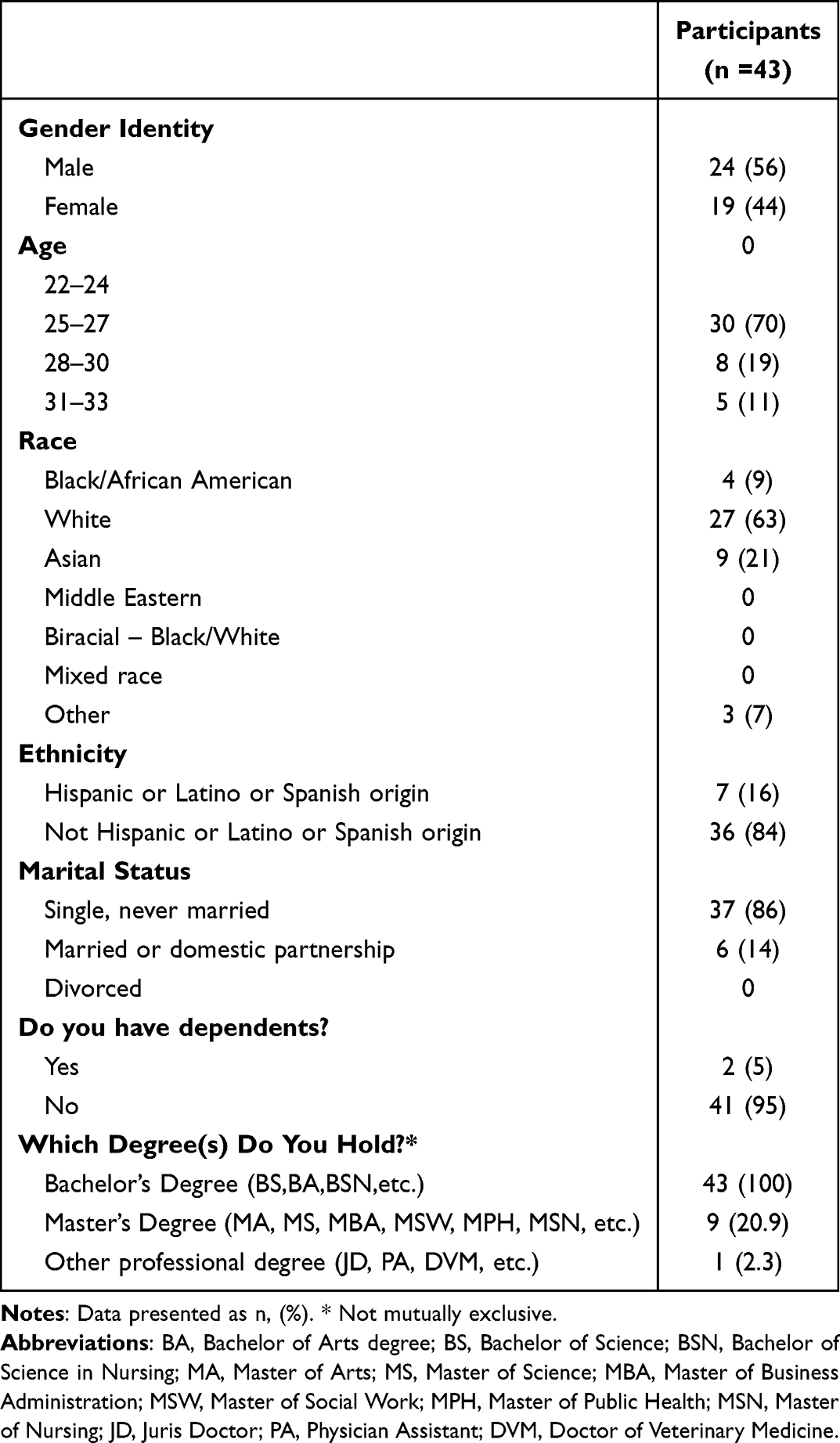

A total of 69 students enrolled into the personal finance workshop and all completed the pre-workshop survey. Forty-three students completed the post-workshop survey 6 months later with a 62.3% response rate and were included in the final analysis. The demographic representation of survey participants is shown in Table 1. Of the 43 participants, 56% were male and 63% were female. A majority of the participants were between the ages 25 to 27 years old and identified as single.

|

Table 1 Demographics of Study Participants |

Basic Personal Finance

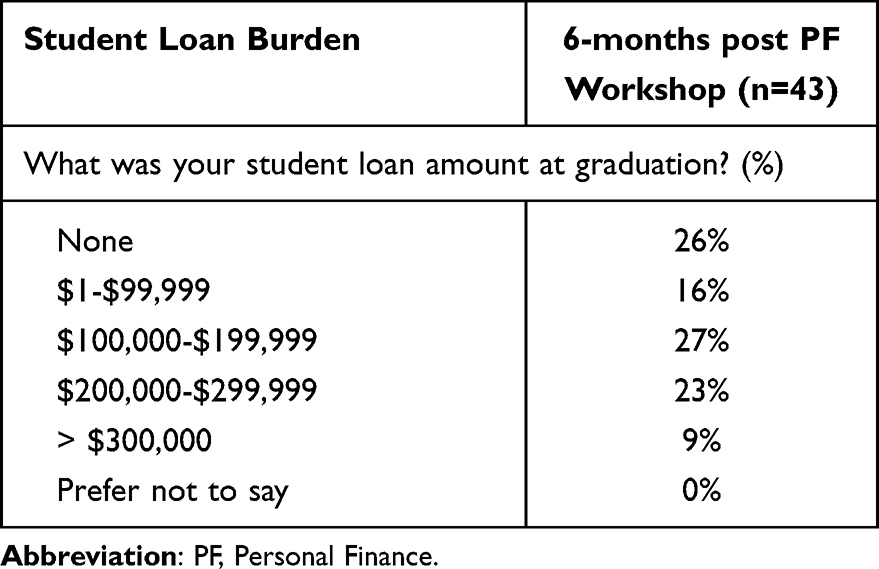

The basic personal financial milestones reported from respondents 6 months after attending the workshop are presented in Table 2. Most of the students in our cohort had recently checked their credit scores, established an emergency fund, and 53% had retirement savings accounts during or prior to starting residency training. Majority of the students achieved basic financial milestones 6 months after the workshop including opening or contributing to a Roth IRA (58%) and contributing to employer sponsored retirement accounts (67%). Thirty-two percent of respondents graduated medical school with >$200,000 of education debt (Table 3). Overall, the financial literacy scores prior to attending the workshop were 54% and improved to 62% 6 months after completion of the workshop (p = 0.004, Figure 1).

|

Table 2 Basic Personal Finance Engagement and Financial Milestones in Residency of Participants 6 Months After the PF Workshop |

|

Table 3 Student Loan Burden of PF Workshop Participants at Graduation |

|

Figure 1 Financial literacy scores before attending the PF workshop and 6 months post-workshop. Number of questions correct were analyzed using paired t-test. Abbreviations: PF, Personal Finance. |

Consensus Surrounding Financial Topics

The final section of the survey inquired about students’ subjective sentiment regarding personal finance topics (Figure 2). Overall, 6 months after the workshop, more students agreed with statements regarding confidence about personal finance knowledge (16% vs 44%, p = 0.024), personal finance as a source of significant stress (65% vs 49%, p = 0.295) and subjective understanding of retirement savings (7% vs 51%, p < 0.001).

|

Figure 2 Graph of pre- and post-workshop results for each of the five consensus questions surrounding financial topics. Students felt more confident about their personal finance knowledge and savings for retirement. The participant response was analyzed using a Chi-square test of Independence. Abbreviations: PF, Personal Finance. |

Discussion

This study demonstrates the feasibility of implementing a basic personal finance workshop for senior medical students. Workshop participants demonstrated an improvement in basic financial literacy 6 months later which led to effective utilization of basic financial tools during the first year of residency.

There is a clear need for a basic personal finance education for medical students. This study is the first to objectively measure financial literacy in senior medical students. Prior studies have only examined the subjective understanding of various financial topics in medical students.10–13 However, a number of previous studies have examined the objective financial literacy of residents and fellows.

Ahmad et al reported a 52% personal finance literacy score among residents and fellows at two different institutions that used modified questions similar to the ones used in our study.10 Rupp et al showed an improvement in financial literacy scores from 50% to 62% in emergency medicine residents after a total of 3 hours of lectures over 6 months.14

In our study, the mean pre-workshop literacy score was 54%, which is similar to prior studies. The mean literacy scores improved to 62%, 6 months after course completion. Students appeared to have good baseline knowledge of the broader financial aspects such as savings accounts, mortgage payments and inflation but lacked a deeper understanding of concepts such as the various types of stock funds, bonds, and taxes. In addition, the majority (68%) of the respondents opened and/or contributed to retirement savings accounts since completion of the workshop. We surmise that the workshop exposed students to the basic financial topics and encouraged them to seek additional information on topics relevant to each individual. This may also have contributed to the improved literacy and engagement with basic financial tools.

Students’ subjective sentiments surrounding financial topics revealed some interesting results. Six months after attending the workshop, more students “agreed” or “strongly agreed” with the statements regarding, “…confidence about my personal finance knowledge and skill” (44% post-workshop vs 15% pre-workshop, p = 0.024) and “…good general knowledge regarding savings and retirement” (51% post-workshop vs 7% pre-workshop, p < 0.001). However, there was a less significant change in the statement “…prepared to deal with student loans” (32.% post-workshop vs 25% pre-workshop, p = 0.171). This was likely due to the fact that the federal COVID-19 student loans payment pause was still in effect during the duration of this study. The participants had not yet started any federal student loan payments and thus were less likely to have engaged in developing student loan management plans. The initial limited subjective knowledge about basic personal finance knowledge including savings and retirement is consistent with the fact that medical students receive minimal personal finance education in their curriculum. At the start of residency, they are required to engage with employer benefits within the first month where they encounter topics such as retirement accounts and various types of savings accounts and are given a crash course on the topic. In addition to the students having to research their own benefits, our course prior to graduating likely better prepared the students to handle open enrollment. These factors likely contributed to the significant improvement in subjective knowledge seen 6 months after the workshop. Regardless, over 90% of the participants agreed or strongly agreed with the statement that, “a personal finance education should be included as part of the medical school curriculum”, highlighting the needs of students and validating efforts such as this workshop.

There are some limitations to this study. The study was performed at a single medical school and the financial workshop was a one-time event, which limits its generalizability. While many of the important topics were covered, a comprehensive review of personal finance topics requires a curriculum spread over multiple sessions. There is a degree of selection bias in our sample as the IPC workshop is an elective that students choose to enroll into. It is possible that students with more interest towards personal finance topics may have been more likely to enroll in this course. The follow-up survey was administered 6 months after attending the workshop in which the length of time from attending the course and self-reported data may lead to a risk of recall bias.

Conclusion

Financial literacy education is limited and essential in any medical school curriculum. Our results have demonstrated that implementation of a basic personal finance workshop for fourth year medical students leads to an objective improvement in basic personal finance literacy. Furthermore, the students demonstrated improved subjective knowledge and comfort with personal finance topics as well as evidence of achieving basic personal finance milestones at the start of residency. Although participants in the course possess some basic knowledge of personal finance, we intend to offer additional resources on different types of equity funds and the effects of taxes and inflation on investment returns to improve their understanding of these financial concepts. Due to our positive feedback, we plan to continue offering the financial literacy course to fourth-year students and aim to expand its reach to preclinical medical students making basic finance education more accessible.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Hanson M. “Average Medical School Debt” EducationData.org,

2. Jayakumar KL, Larkin DJ, Ginzberg S, Patel M. Personal Financial Literacy Among U.S. Medical Students. MedEdPublish. 2017;6:35.

3. Grewal K, Sweeney MJ. An Innovative Approach to Educating Medical Students About Personal Finance. Cureus. 2021;13(6):e15579. doi:10.7759/cureus.15579

4. Medical School Graduation Questionnaire. AAMC. Availabe from: https://www.aamc.org/data-reports/students-residents/medical-school-graduation-questionnaire.

5. Panagioti M, Panagopoulou E, Bower P, et al. Controlled Interventions to Reduce Burnout in Physicians. JAMA Intern Med. 2017;177(2):195. doi:10.1001/jamainternmed.2016.7674

6. Connelly P, List C. The Effect of Understanding Issues of Personal Finance on the Well-being of Physicians in Training. WMJ. 2018;117(4):164–166.

7. West CP, Shanafelt TD, Kolars JC. Quality of Life, Burnout, Educational Debt, and Medical Knowledge Among Internal Medicine Residents. JAMA. 2011;306(9):952–960. doi:10.1001/jama.2011.1247

8. Bui D, Winegarner A, Kendall MC, et al. Burnout and depression among anesthesiology trainees in the United States: an updated National Survey. J Clin Anesth. 2023;84:110990.

9. FINRA. The Financial Industry Regulatory Authority, Inc. https://www.finra.org.

10. Ahmad FA, White AJ, Hiller KM, Amini R, Jeffe DB. An assessment of residents’ and fellows’ personal finance literacy: an unmet medical education need. Int J Med Educ. 2017;8:192–204. doi:10.5116/ijme.5918.ad11

11. Gilbert J, Kothari P, Sanchez N, Spencer DJ, Soto-Greene M, Sánchez JP. Is Academic Medicine a Financially Viable Career? Exploring Financial Considerations and Resources. Mededportal. 16. doi:10.15766/mep_2374-8265.10958

12. Liebzeit J, Behler M, Heron S, Santen S. Financial literacy for the graduating medical student. Med Educ. 2011;45(11):1145–1146. doi:10.1111/j.1365-2923.2011.04131.x

13. Meleca JB, Tecos M, Wenzlick AL, Henry R, Brewer PA. A medical student initiated elective course in business and finance: a needs analysis and pilot. Med Stud Res J. 2014;4:18–23.

14. Rupp SL, Abramoff C, McCloskey K. Efficacy of Peer-to-Peer Education for Emergency Medicine Resident Financial Literacy: curriculum Development Study. Cureus. 2022;14(12). doi:10.7759/cureus.32668

© 2024 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms.php

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2024 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms.php

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.